Is ILOE Insurance Mandatory? Category A vs B Explained

ILOE is the UAE’s mandatory unemployment insurance scheme. It is compulsory for most private-sector and federal-government employees, who must subscribe within four months of their work permit being issued. Your category depends only on your basic salary: Category A (AED 16,000 or below) costs AED 5 a month plus VAT, and Category B (above AED 16,000) costs AED 10 plus VAT.

What is ILOE insurance?

Involuntary Loss of Employment (ILOE) is the UAE’s unemployment insurance scheme, launched in January 2023. It gives employees who lose their job through no fault of their own a temporary cash benefit while they look for new work. The Ministry of Human Resources and Emiratisation (MOHRE) runs the scheme, and Dubai Insurance Company underwrites it on behalf of an insurance pool. You may also see it called job-loss insurance or the unemployment insurance scheme.

ILOE is not health insurance, and it is not the same as your end-of-service gratuity. Those are separate entitlements. ILOE does one specific thing: it pays a portion of your salary for a short period if you are made redundant or terminated, provided you have kept the cover active.

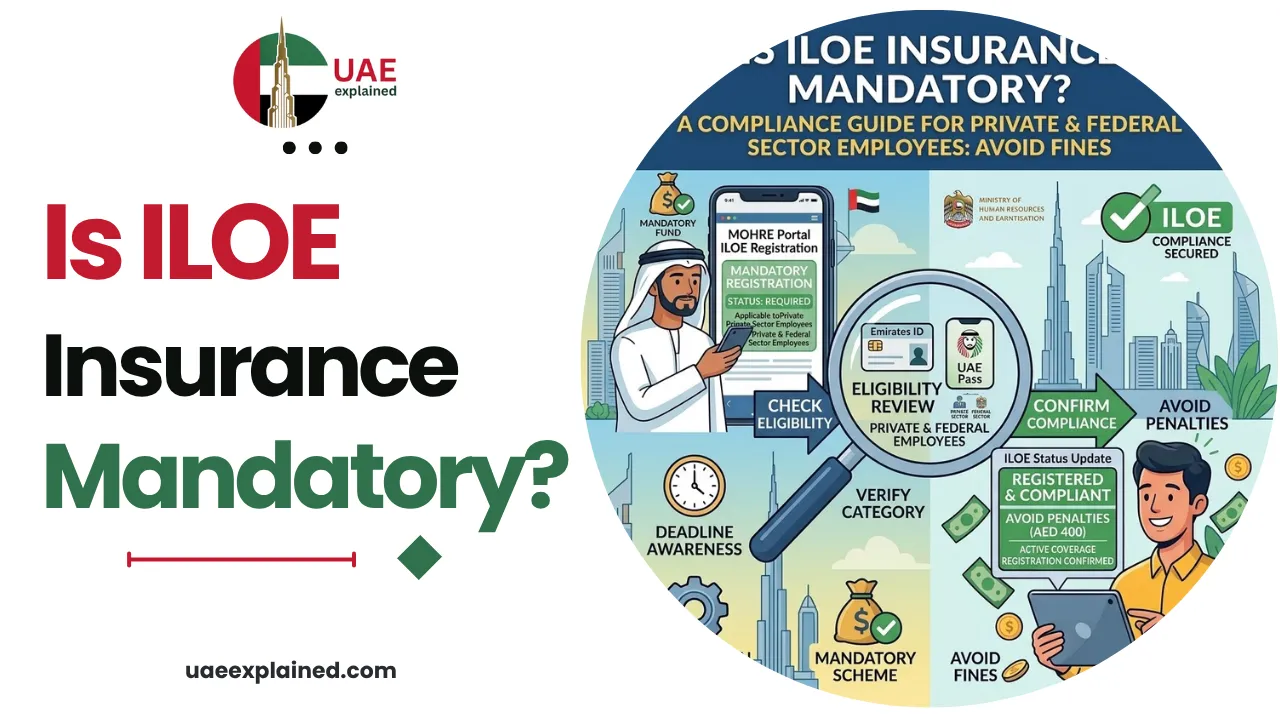

Is ILOE insurance mandatory?

Yes. Since January 2023, ILOE has been compulsory for private-sector and federal-government employees, both Emirati and expatriate, and the requirement was extended to free-zone and semi-government employees in May 2023. If you are an eligible employee, you must subscribe within four months of your work permit being issued, and keep the cover active by paying your premium on time.

There are exceptions. Certain workers are exempt entirely (see below), and the financial free zones DIFC and ADGM operate their own arrangements, where participation can be voluntary. If you work for a local-government entity or one of those financial free zones, confirm your own status rather than assuming, because the rules there can differ from the federal scheme. Not subscribing when you should triggers a fine, see our guide to the ILOE fine check and payment.

Who must subscribe and who is exempt

The simplest way to know where you stand is to find your group in the table below. Note that exempt workers cannot join the scheme even if they want to.

| Group | ILOE status |

|---|---|

| Private-sector employees (Emirati & expat) | Must subscribe |

| Federal-government employees | Must subscribe |

| Free-zone & semi-government employees | Must subscribe |

| Investors / owners of the company they work in | Exempt |

| Domestic workers | Exempt (separate framework) |

| Temporary-contract workers | Exempt |

| Workers under 18 | Exempt |

| Pensioned retirees who take a new job | Exempt |

| DIFC / ADGM employees | Own rules, often voluntary; check your status |

Category A vs Category B

If you must subscribe, your premium and your maximum payout are set by your category, and your category is set by one number: your basic monthly salary.

| Category | Your basic salary | Monthly premium | Maximum monthly payout |

|---|---|---|---|

| Category A | AED 16,000 or below | AED 5 + VAT | AED 10,000 |

| Category B | Above AED 16,000 | AED 10 + VAT | AED 20,000 |

The figure that matters is your basic salary as written in your employment contract and on your payslip, not your gross pay. Allowances, housing, transport, and commission are excluded, so a worker on an AED 12,000 basic plus AED 6,000 in allowances is still Category A. That single rule decides both your premium and the cap on any future claim.

If a raise or new contract pushes your basic salary above AED 16,000, move up to Category B. Staying on Category A leaves you under-insured, a claim would pay only the lower AED 10,000 cap.

What you pay and what you get

The trade is a small premium for a meaningful safety net. For AED 5 or AED 10 a month, an active subscription pays 60% of your average basic salary for up to three months if you lose your job involuntarily, capped at your category limit. To benefit, you need at least 12 continuous months of cover, which is why keeping the policy active matters as much as having it.

From here, the practical steps live on their own pages: how to subscribe to or renew your ILOE insurance, and, if you have lost your job, how to claim your ILOE benefit. You will find the whole cluster, and the rest of UAE employment, in our UAE work and labour guide.

Frequently asked questions

Is ILOE insurance mandatory in the UAE?

Yes, for most employees. ILOE has been compulsory since January 2023 for private-sector and federal-government workers, and since May 2023 for free-zone and semi-government employees. Eligible workers must subscribe within four months of their work permit. Investors, domestic workers, temporary-contract staff, under-18s, and pensioned retirees in new jobs are exempt.

How do I know if I am Category A or Category B?

Look at your basic salary, not your gross pay. If your basic monthly salary is AED 16,000 or below you are Category A; above AED 16,000 you are Category B. Allowances, housing, transport, and commission do not count. The category sets both your AED 5 or AED 10 premium and your AED 10,000 or AED 20,000 payout cap.

Is ILOE the same as end-of-service gratuity?

No. End-of-service gratuity is a lump sum your employer pays when your employment ends, based on your length of service. ILOE is a separate insurance scheme that pays a monthly benefit for up to three months only if you lose your job involuntarily and have kept the cover active. You can receive both, as they are unrelated.

What happens if I do not subscribe to ILOE?

If you are required to subscribe but do not, you are charged an AED 400 fine, and an unpaid fine can block a new work permit. Letting premiums lapse for more than three months adds a separate AED 200 fine and can cancel your cover. Subscribing on time avoids both and keeps you eligible to claim.

Last verified: June 2026

Reviewed by: UAEexplained editorial team

Source: ILOE (Dubai Insurance Company); Ministry of Human Resources and Emiratisation (MOHRE)